By Chuck Black

It passed virtually unnoticed when it was first released in September 2017. But the 2015 State of the Canadian Space Sector Report, the latest in a series of annual Canadian Space Agency (CSA) assessments of our domestic space industry, is well worth revisiting to prepare for any new announcements the current Liberal government under Prime Minister Justin Trudeau might make between now and when the next Federal budget is released in March 2018.

As outlined in the executive summary, "In 2015, total revenues in the Canadian space sector totalled $5.3Bln CDN, representing a slight decrease overall of 1.6%, or $85Mln CDN, year-over-year. The average annual growth rate of the space sector over the last five years (2010–2015) is relatively flat at 0.4%."

In a surprise finding, the report concluded that university and research centre revenues amounted to only $125Mln CDN in 2015, or only 2.4% of the total revenue measured, although six universities were included in the list of Canada’s top 30 space organizations.

According to the report:

Now that this longstanding perception has been disproved, it will be interesting to see if the new knowledge ends up making any real difference.

As well, the total Canadian space workforce (excluding government workers) "totaled 9,927 space-related full-time equivalents (FTEs) in 2015. This represents a very slight decrease (less than 1% change) from the figure reported last year, 10,012 FTEs."

According to the report:

It's also useful to note the amount of private sector money going into research and development. As outlined in the report:

Taken together the data collected in the report suggests a space industry driven by industry, not academia or government.

To be fair to the other two, it so far looks like industry hasn't yet made it clear where it wants to go and maybe each individual business just wants the ability to go its own way.

However, and as outlined in the February 15th, 2010 post, "Ottawa Citizen: 'Where did that Long Term Space Plan Go?'," this blog once suggested that, "if Canada does not define a long term space plan, private business and academia will soon go about creating their own."

That day has arrived. Welcome to the future.

Chuck Black is the editor of the Commercial Space blog.

It passed virtually unnoticed when it was first released in September 2017. But the 2015 State of the Canadian Space Sector Report, the latest in a series of annual Canadian Space Agency (CSA) assessments of our domestic space industry, is well worth revisiting to prepare for any new announcements the current Liberal government under Prime Minister Justin Trudeau might make between now and when the next Federal budget is released in March 2018.

|

| The front cover of the 2015 State of the Canadian Space Sector Report and it's core finding. In essence, our domestic space industry has been in a state of stagnation for the last five years with growth at a "relatively flat" 0.4% annually. Graphics c/o CSA. |

As outlined in the executive summary, "In 2015, total revenues in the Canadian space sector totalled $5.3Bln CDN, representing a slight decrease overall of 1.6%, or $85Mln CDN, year-over-year. The average annual growth rate of the space sector over the last five years (2010–2015) is relatively flat at 0.4%."

Essentially, this means that the Canadian space sector spent the period between 2010 - 2015 in a five year slump.

But the Canadian revenues are in line with international markets. As outlined in the July 2016 Edition of the Space Report, published annually by the Denver CO based Space Foundation:

But the Canadian revenues are in line with international markets. As outlined in the July 2016 Edition of the Space Report, published annually by the Denver CO based Space Foundation:

The global space industry grew in 2015, although currency fluctuations caused the appearance of a decline from $329Bln US ($418Bln CDN) in 2014 to $323Bln US ($410Bln CDN) in 2015.

Due to the strong US dollar and the ever-increasing levels of activity outside the United States, these fluctuations have a more noticeable impact than would have been the case in previous decades when the US share of the commercial space industry was larger.

|

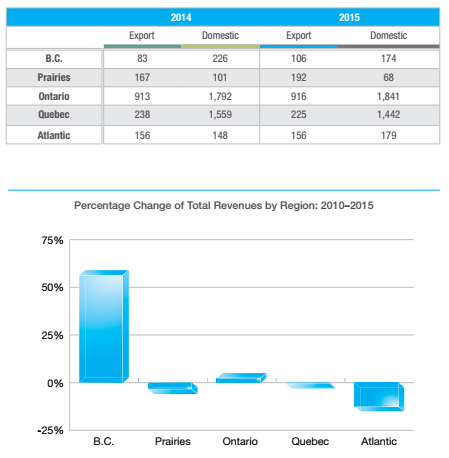

| If nothing else, the west coast seems to have weathered the slump far better than the rest of the country. Although revenue dipped 9% in 2015, "between 2010 and 2015, BC’s total revenues increased by 59%, from $177Mln CDN to $281Mln CDN. This growth has been driven by domestic revenue sources, which have increased from $81Mln CDN to $174Mln CDN, while export revenues increased slightly from $95Mln CDN to $106Mln CDN, over the same period." Richmond, BC based MacDonald Dettwiler (now San Francisco, CA based Maxar Technologies) was the largest Canadian space company in BC during this period. Graphic c/o CSA. |

In a surprise finding, the report concluded that university and research centre revenues amounted to only $125Mln CDN in 2015, or only 2.4% of the total revenue measured, although six universities were included in the list of Canada’s top 30 space organizations.

According to the report:

Academic organizations contribute 20% of the total space sector workforce with 1,997 full-time equivalents, of which 55% are highly qualified personnel (HQP) such as engineers, scientists and technicians.

An additional 40% of the university and research centre workforce is comprised of students, mostly at the graduate level, who are in receipt of wages or a stipend from their university for work as research assistants, teaching assistants, or other employee-type situations.The general consensus until now has been that Canadian academics (with funding from government through the CSA, the National Research Council and from a few of the bigger space companies) essentially drive the space industry.

Now that this longstanding perception has been disproved, it will be interesting to see if the new knowledge ends up making any real difference.

|

| Revenue growth and proportion by activity sector during the period 2010 - 2015. It's worth noting that, while satellite communication is the largest sector by revenue ($4.5Bln CDN for 2015), the Earth observation (EO) market segment is the fastest growing. As outlined in the report, "Over the past five years, EO revenues have increased by 65%, from $256M in 2010 to $423M in 2015, growing on average 11% annually." Graphic c/o CSA. |

As well, the total Canadian space workforce (excluding government workers) "totaled 9,927 space-related full-time equivalents (FTEs) in 2015. This represents a very slight decrease (less than 1% change) from the figure reported last year, 10,012 FTEs."

According to the report:

In 2015, engineers and scientists comprised the largest category of employment with 2,953 FTEs, representing 30% of the total space workforce.

Employees in the administration category made up the second largest group with 2,911 FTEs and 29% of the total workforce.

Technicians came third with 1,311 FTEs and 13% of the total workforce.

Management, marketing and sales, and other employees made up the remainder.

|

| A chart showing Canadian space industry revenue growth from 2007 - 2011 with a slump in growth after 2011. Graphic c/o CSA. |

It's also useful to note the amount of private sector money going into research and development. As outlined in the report:

In 2015, there were 67 companies engaged in R&D activities. Total spending was $256Mln CDN, a significant increase over R&D spending reported in 2014 ($146Mln CDN). Upstream organizations were more R&D intensive, spending 55% of total space sector BERD (business enterprise research and development).

R&D spending was financed through internal sources (e.g. company profits reinvested in R&D) or through external funding sources (e.g. government grants and contributions).

Internally company-funded R&D represented the larger portion of spending at $139M or 54% of BERD in 2015. Externally funded R&D represented 46%, or $117M, of BERD in 2015.The $256Mln CDN spent by corporations in 2015 was twice the $125Mln CDN revenue spent at University and research centre. According to the report:

Universities and research centres received $115.6Mln CDN in domestic funds, mostly from government: $91.6Mln CDN from the federal government and $14.7Mln CDN from provincial governments. The remainder came from private foundations or companies (or foreign sources of funding).

|

| Domestic vs export revenue for the Canadian space industry in 2015. Graphic c/o CSA. |

Taken together the data collected in the report suggests a space industry driven by industry, not academia or government.

To be fair to the other two, it so far looks like industry hasn't yet made it clear where it wants to go and maybe each individual business just wants the ability to go its own way.

However, and as outlined in the February 15th, 2010 post, "Ottawa Citizen: 'Where did that Long Term Space Plan Go?'," this blog once suggested that, "if Canada does not define a long term space plan, private business and academia will soon go about creating their own."

That day has arrived. Welcome to the future.

|

| Chuck Black. |

___________________________________________________________

No comments:

Post a Comment